A car insurance deductible is the amount you pay out of pocket before your car insurer begins to be. Car insurance deductibles are only relevant for certain types of insurance coverage, but it is very important to understand how car insurance deductibles work before you file a claim. In this article, we address the most common questions related to car insurance deductibles and help you decide when to make a claim!

Table of Contents

How does a car insurance deductible work?

A car insurance deductible is the amount that you pay out of pocket before your car insurance company begins paying. Put simply, the cost of the damage to your car, less your deductible, is the amount that your car insurance company will pay out. It’s important to remember that you will always pay your full deductible before your car insurance company pays anything.

Is my car insurance deductible per claim or per year?

Car insurance deductibles are enforced per claim. This means that even if you’ve had multiple incidents in a year, you will still need to pay the full deductible each time you make a new claim. This is very different than health insurance, where you have an annual deductible you will need to meet before your insurance begins paying.

Should I make a claim below my deductible?

No, you typically should not make a car insurance claim that is below your deductible. As we’ve mentioned, deductibles work on a per claim basis, so making a claim will not have any impact on the future deductibles you will need to pay. Making a claim will take time and will likely result in an increase in your car insurance rates. A claim below your deductible is just not worth it!

Which types of car insurance coverage have a deductible?

Typically, comprehensive and collision insurance coverages will have a deductible. Comprehensive and collision insurance both protect your car from incidents (such as hail or hitting a deer), but they do not protect you (the driver) or your liability if you injure another driver or damage their car. In some states, it is also common to have deductibles for other coverages, such as personal injury protection or underinsured/uninsured motorist protection. You will also find that your liability coverage will never have a deductible.

Why do collision and comprehensive car insurance have a deductible?

Collision and comprehensive insurance have a deductible because insurers do not want drivers making a claim for small incidents. Because these coverages impact your car and not other drivers, it is your choice whether or not you make a claim. Insurance companies require drivers to pay a deductible in order to be sure drivers only make claims for substantial damage.

It is important to note that deductibles don’t exist just because car insurance companies do not want to pay claims to their policyholders. Car insurance companies spend money to process claims, such as paying a body shop to review the damage or an adjuster to inspect your car. These costs are generated whether the damage to your is large or small. If deductibles did not exist, drivers could make constant frivolous claims and greatly increase costs for insurance companies. These costs would get inevitably passed on to other drivers, increasing the cost of insurance for everyone!

Why doesn’t liability car insurance have a deductible?

Deductibles are in place to align the interests of drivers and their insurance companies. Liability coverage protects other drivers from your actions, so there is no opportunity for drivers to file frivolous claims and no opportunity to align interests. If you collide with another driver they should receive full payout from your car insurance company, regardless of whether the collision causes a small amount of damage or a lot of damage.

How do you find your car insurance deductible?

Your car insurance deductible is easy to find either directly in your policy, through your car insurer’s online portal, or from your insurance agent. You will usually see that collision and comprehensive coverages will typically only list your deductible, rather than the limit (since both policies have a limit equal to the cost of your car).

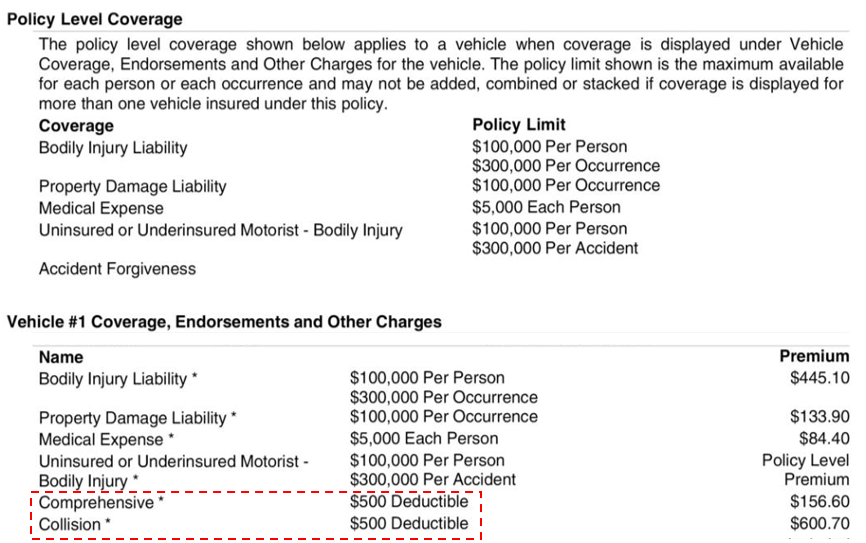

Below is an example of where to find your deductible in your policy materials (based on a sample American Family Insurance policy).

Do you pay your car insurance deductible if you are not at fault?

If you are deemed not at fault in an accident you typically won’t need to pay your deductible. When you are the victim in an accident you can still use your collision insurance, but your insurer will seek repayment from the other driver’s insurance company for both your deductible and any payouts the insurer makes.

The exception, however, is when the other driver has no insurance or is underinsured. If you have uninsured motorist coverage with a deductible, you will need to pay the deductible before your coverage kicks in.

How large should my car insurance deductible be?

The size of your deductible is determined by your tolerance for risk and ability to fund a deductible. Selecting the size of your deductible is usually a trade-off between your monthly rate and the size of one-time payments you can afford. The average car insurance deductible is around $500. This is usually the right-size deductible for most drivers, however, you may want to consider higher or lower deductible depending on your specific circumstances:

- You may want a lower deductible if… you can’t afford a large one-time payment. A lower deductible will allow you to avoid a large one-time payment in the event of an accident, but in exchange, you will pay more per month for your insurance.

- You may want a higher deductible if… you want to lower your monthly insurance rate. Increasing the size of your deductible can be a great way to reduce the cost of your insurance as long as you feel like you can afford the one-time payment.