How each car insurance company prices its policies is a closely guarded secret. Most car insurers have teams of data scientists that are constantly tweaking their algorithms to determine the perfect price to sell car insurance to each person (these algorithms collectively are an insurance company’s “pricing model”). Because insurers intentionally hide their pricing models from the public, it can be difficult to identify why these differences exist. However, although each pricing model is unique, most insurers have several similarities that we will discuss in detail below.

Table of Contents

How do traditional car insurance pricing models work?

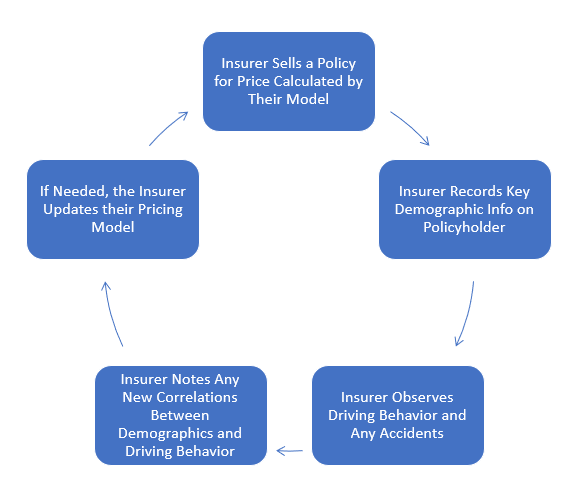

Pricing models are designed to digest your driving “fingerprint” and attempt to calculate the perfect price that the car insurance company should charge you. In developing this price model, the insurance company will review all of their historical data and try to identify correlations between driver characteristics and the likelihood a driver will make a claim (i.e. get in an accident). When an insurance company thinks it has found a correlation, the insurance company will then update its pricing model. Consider an example below.

One day an insurance company’s data scientist is reviewing historical data and they find that people driving red cars are twice as likely to get into a severe accident than those driving any other car. The data scientist investigates further and finds that, indeed, it seems that those who drive red cars drive faster and more aggressively than the average person and do get into more accidents. The data scientist decides to make a tweak to the pricing model and the insurance company begins charging a higher price to those with red cars.

The red car situation above, is an example of the constant pattern recognition and price updating insurance companies go through each day. The constant data review and price updating create a feedback loop that results in constant price changes.

The Car Insurance Pricing Feedback Loop

What are the common driver details that car insurance companies use?

Many insurance companies use similar data points in their pricing models, including:

- Age

- Marital Status

- Credit Score

- Location

- Accident History

- Ticket History

Although many of these many insurance companies will use these similar data points, they each will place a slightly different weighting on these metrics. These slight differences in models are what cause you to get different quotes from each car insurance company!

Why do car insurance companies keep their pricing models secret?

The key input to these pricing models is a car insurance company’s historical driver data. This data is privately owned by each insurance company and likely collected over decades. Without this dataset, it is extremely difficult for a car insurance company to profitably sell insurance. So to prevent new competitors from selling insurance and stealing their customers, car insurance companies keep this data secret.

Further, car insurance is an industry where drivers will purchase insurance at the best price and typically have no brand loyalty. According to a 2021 Value Penguin survey, 76% of drivers have price shopped for insurance. Americans are constantly price shopping and if an insurance company didn’t keep their pricing models confidential, then their competitors could simply offer car insurance at slightly better prices and steal their customers!

New Pricing Models

In addition to the historical pricing models discussed above, with technology advancements insurers are also turning towards novel methods of using technology to price auto insurance.

Telematics

Telematics technologies can be attached to your car or simply downloaded as a smartphone app, and are designed to measure your driving performance. Telematics can measure how often you speed, how reckless your driving behavior is, and how often you have to slam on the breaks. This information helps insurers understand your driving patterns which can lower your insurance rates (or potentially increase them if you drive dangerously!).

Telematics technologies are relatively new and car insurance companies haven’t quite perfected their use. For this reason, even with a telematics tool your pricing is unlikely to change significantly – however, this could change in the future!

Usage-Based Pricing

Usage-based pricing refers to insurance companies pricing insurance by the mile, rather than by the month. The idea behind usage-based pricing is that drivers who are on the road more often are more likely to get into an accident and should consequently be charged more for insurance.

Like telematics, usage-based pricing is a relatively new phenomenon (first popularized by MetroMile in 2013) that only recently became possible with improvements in technology.

External Pricing Factors

In addition to the difference in pricing models above, there are several additional reasons why a car insurance company may have very different pricing than another. These factors are outside of the driver’s control and include:

- A new insurer wants to win over customers: when a new car insurance company is launched, they need to win customers from existing insurers. One way they can do this is by aggressively lowering their prices. Although they will likely lose money in the short term, they are willing to do this in the hope that they can raise rates in the future and retain most of their customers

- An insurer wants to reduce their exposure in an area: insurance companies depend on diversification to reduce their risk. If a company has sold too many policies in a given area they may significantly increase prices (or stop selling policies entirely) until they’ve sold in other areas and their book begins to balance out.

- The insurance company may have had a bad year: when an insurer loses a lot of money in one year (i.e. they pay out a lot of claims), they may need to raise prices significantly to pay for their past losses. Typically loss movement is an industry-wide phenomenon that will raise or lower prices across all insurers (for example, if inflation increases), but sometimes an increase in losses is an isolated incident resulting from issues at a single insurer

Insurance companies are constantly updating their pricing models and tweaking their strategies – this is why we recommend you should be constantly price shopping and getting new quotes. Since your last renewal, an insurance company may have prioritized a new variable in your favor and without receiving a new quote you would never know!