Car insurance companies make money in two ways. The first way your car insurance company makes money is through “underwriting profit”. Put simply, an insurer makes an underwriting profit when they charge drivers more than they pay in claims. The second way they make money is through “investing profit”, which is the profit the insurance company makes from investing excess cash. In this article, we will discuss these two different earnings streams and how changes in each will impact your car insurance rates.

Table of Contents

1. Underwriting Profit

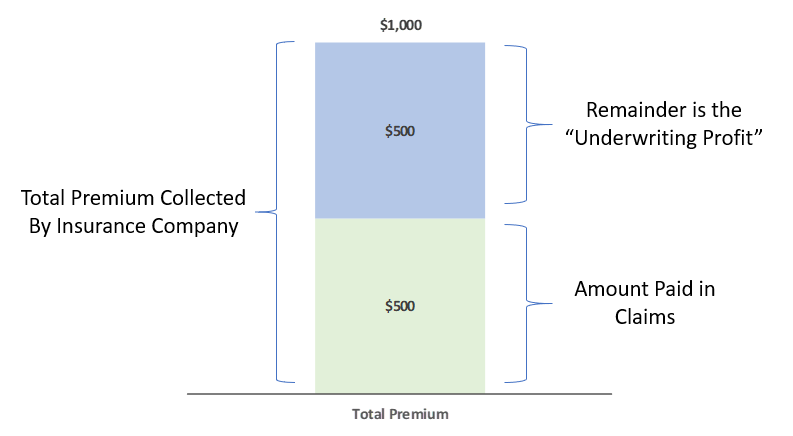

As we’ve mentioned, underwriting profit is the difference between insurance payments the insurance company receives (called “premiums”) and the amount that they pay out, if, for example, someone gets in an accident (this is called a “claim”).

As an example, consider that an insurance company, “InsureCo”, sells a car insurance policy to a car owner, “Bob”, for $1,000. A few months after buying the insurance policy, Bob gets distracted and rear-ends someone causing $500 in damage. InsureCo pays out the $500 to the victim that Bob hit. After this accident, Bob drives much more safely and avoids getting into any other accidents.

In this example, at the end of the year, InsureCo is very happy because they made $500 in “underwriting profit” (the $1,000 that Bob paid, less the amount InsureCo paid to the driver Bob hit).

What factors impact a car insurer’s underwriting profit?

There are many reasons that a car insurer’s underwriting profit decreased (likely causing an increase in insurance prices!), but we walk through three of the most likely reasons below:

- Economic Inflation: when inflation increases, it means that repairs are more expensive and that the insurance company will consequently need to pay more in claims. This can cause the car insurance company to make less money and your rates to potentially increase.

- Social Inflation: social inflation is defined as increased litigation based on societal pressure. Examples of social inflation are aggressive personal injury law firms and a “sue-happy” culture. When social inflation increases – meaning insurers are getting sued more often – car insurers will have to pay more often (and larger) claims. This leads to a decline in underwriting profit and higher rates.

- Catastrophes: if a bad hurricane or hailstorm hits your region, your car insurance company will have to pay out a very large number of claims at once. This can significantly reduce their underwriting profit and raise your rates.

2. Investing Profit

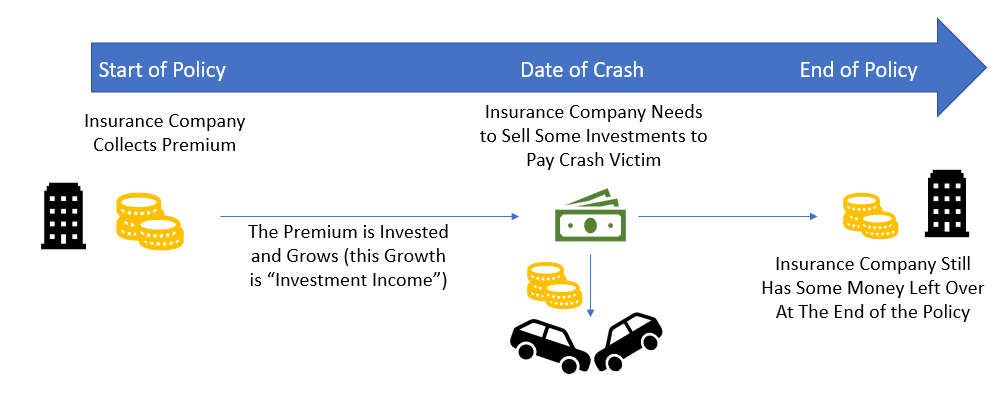

The second way that car insurance companies make money is through investing. Because insurance companies collect premiums from drivers upfront, and only later pay claims (potentially months after the policy is sold), they often have excess cash to invest. Insurance companies take this excess cash and invest it until they need to pay a claim.

Take another example of “Bob” and “InsureCo”. In this example assume that InsureCo again sells Bob an insurance policy for $1,000. Bob again gets distracted and hits a car, but this time Bob causes $1,000 in damage that InsureCo needs to pay.

Because InsureCo collected $1,000 in premium and paid out $1,000 in claims, they made no underwriting profit off Bob’s policy – but they can still make a profit by investing! In this example, as soon as Bob paid InsureCo, InsureCo invested his $1,000 in a bond that pays 10% interest per year (or $100). If Bob didn’t get into an accident until the very last day of his policy, then InsureCo would have made $100, even though they paid out just as much as they took in!

In this example, the car insurance company is still happy and made money even though they paid out just as much as they collected!

What factors impact a car insurer’s investing profit?

Similar to underwriting profit, there are many ways that a car insurance companies investing profit can change. We lay out two of the most likely reasons below:

- Interest Rates: the bulk of an insurance company’s investments are in bonds and other debt instruments which decline in value when interest rates increase (see: an article on Investopedia for an overview on how interest rates impact the value of bonds). The change in the value of these bonds and debt investments impacts an insurer’s investment income and may result in an increase (or decrease) in your car insurance rates.

- Investment Decisions: most often, car insurance companies are investing in low-risk securities (and in fact, are required to do so by the state). However, car insurance companies do have some leeway to select exactly what to invest in. If an insurance company makes a good (or bad) investment decision that can impact their investment income and potentially your rates.

Conclusion

In order to keep the lights on and pay all their other costs, insurers need to continuously make a profit through some combination of underwriting and investing profits. Understanding how an insurance company makes money can be very helpful to put in context why your rates are being raised (or to help predict when a rate rise will be coming).